Catalog Acquirers: Six Archetypes for a Two-Tier Market

The market for music catalog acquisitions can no longer be understood through the old three-tier hierarchy—major labels, specialized funds, niche players. Three developments have rendered it obsolete.

This article is the second in a seven-part series drawn from the exclusive investigation “Music Catalog Acquisitions 2026” by @music_zone. The full investigation (~45 pages, PDF) gives a complete view of the 2024–2026 cycle: Hipgnosis/Recognition, the new acquirer archetypes, the Shot Tower / Music Finance Index multiples, AI and ancillary rights, non-anglophone geographies, and the concentration risks across capital / collection / catalog.

Get the full investigation as a PDF ($59)

Between the rise of a global-scale independent with BMG-Concord, the majors’ growing recourse to joint ventures backed by institutional capital, and the financialization of the U.S. collective management organizations, the map of buyers has grown more complex and more vertical.

A new map of the market

The historical reading of the market distinguished three groups: the majors at the top, the specialized funds in the middle, then a fragmented periphery of opportunistic acquirers. This grid no longer suffices to describe the 2025–2026 landscape, because three developments have rendered it partly obsolete: the BMG-Concord combination, the rise of major / institutional-capital joint ventures, and the passage of several U.S. collective management organizations under investment-fund control.

The decisive point is that buyers are no longer distinguished by size alone, but along two more useful axes: the financial logic of the vehicle — strategic, financial or hybrid — and the operating intensity exercised on the acquired catalogs, from passive ownership to integrated marketing exploitation. It is this dual reading that today explains why very different players can find themselves facing one another over the same assets, while targeting distinct returns, holding horizons and industrial uses.

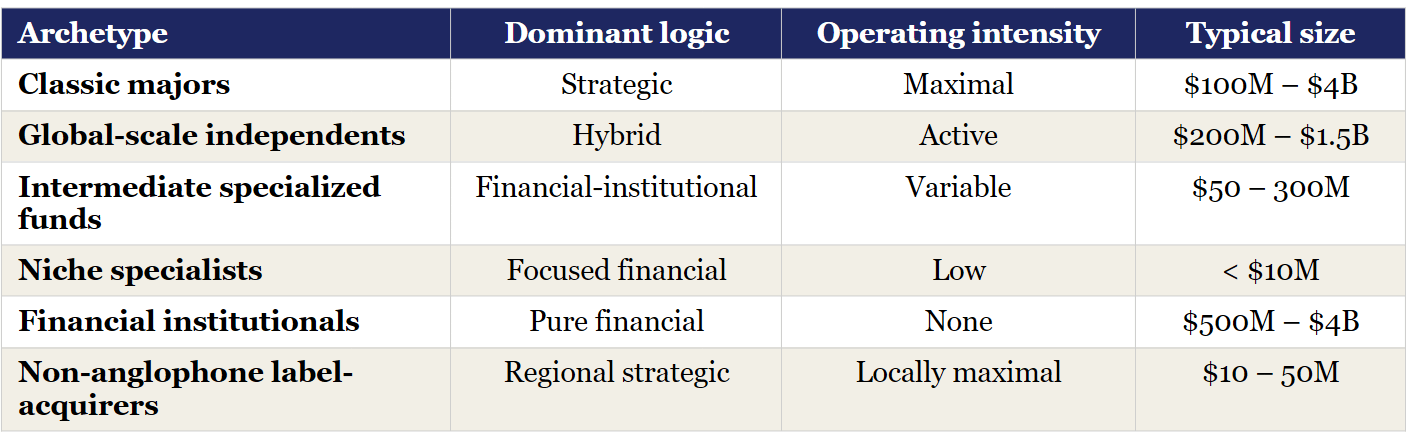

The six archetypes

The 2026 mapping brings six families of acquirers into focus.

The classic majors — Universal, Sony and Warner — remain the most integrated operators in the market, with maximal capacity in administration, marketing, synchronization and platform negotiation. Per the Music & Copyright estimates cited in the investigation, they concentrate about 60% of global publishing and 67% of recordings, but their acquisition mode now splits between their own balance sheet and third-party-backed vehicles above a certain threshold.

The global-scale independents constitute the new archetype. BMG-Concord, valued at about 14 billion dollars per Bloomberg, reaches a scale that Variety describes as that of a “potential fourth major,” while the Primary Wave-Kobalt whole approaches this category with about 7 billion dollars in combined assets after the announced acquisition of Kobalt by Primary Wave.

The intermediate specialized funds — HarbourView, Litmus, Influence Media, Iconic Artists Group, Pophouse — occupy the middle of the market. They combine institutional capital, sector selectivity and variable operating intensity, often with a major’s support for distribution or administration.

The niche specialists, for their part, target the long tail and small tickets. The Duetti-Billboard Music Finance Index shows, moreover, that the growth sentiment is strongest on transactions below one million dollars and between one and five million, which reinforces the picture of a market very active at the base while consolidation concentrates at the top.

The financial institutionals — Blackstone, Apollo, Brookfield, Bain, GIC, KKR — exercise no direct operating intensity on the works, but structure the economic ownership of the rights and the cost of capital. Blackstone’s path on Hipgnosis and then Recognition illustrates this role: acquire a discounted asset, refinance it and arbitrage it at exit to a strategic buyer.

Finally, the non-anglophone acquirers are no longer a mere exotic supplement to the Western market. In the investigation, they split between South Asian label-acquirers such as Saregama, Tips Music or T-Series, and East Asian platform-acquirers such as HYBE/Weverse, SM/DearU or Tencent Music, which articulate rights, superfan platforms and direct exploitation of the fan relationship.

The real turning point: the majors split in two

The most structuring change is not the return of big deals, but the transformation of the vehicle that carries them. For very large acquisitions, the majors have stopped relying exclusively on their balance sheets and now turn to hybrid co-investment structures with long-term institutional capital.

Three models dominate as of mid-2026. Sony-GIC, formed in January 2026, embodies the major / sovereign-fund model with 2 to 3 billion dollars of initial capital and serves as the vehicle for the Recognition acquisition. Warner-Bain, announced in July 2025 and then raised to 1.65 billion dollars in February 2026, rests on private-equity capital with a shorter exit horizon and has already served to acquire the Red Hot Chili Peppers’ recorded-music catalog for more than 300 million dollars. Universal-Chord, finally, operates as an externalized platform in which Universal is a minority holder but captures the administration and the operating value.

This shift profoundly alters the structure of power in the market. The majors retain industrial control of the catalogs, but a growing share of the economic ownership of the rights is carried by sovereign capital, permanent capital or private equity. In other words, operating concentration remains musical, while capital concentration becomes financial.

BMG-Concord and Primary Wave-Kobalt: the rise of the quasi-majors

Two deals sum up the recomposition of the middle tier. The BMG-Concord merger announced on April 28, 2026 creates a player valued at about 14 billion dollars, with a capital structure of 67% for Bertelsmann and 33% for Great Mountain Partners and pro forma EBITDA above 730 million dollars per the information reported by Bloomberg and relayed by the trade press. This scale places the whole in a category distinct from that of mere catalog funds.

For its part, Primary Wave announced on March 23, 2026 the acquisition of Kobalt in a deal valuing the target at around 1.5 billion dollars and the combined entity at around 7 billion. This deal, backed by Brookfield, confirms that an independent can now aggregate publishing, technology, digital collection via AMRA and a rights portfolio at a scale nearly equivalent to that of the majors on certain segments.

These two combinations do more than swell balance sheets: they change the market’s vocabulary. The “specialized funds” tier no longer suffices to describe structures capable of administering at scale, negotiating with platforms and absorbing the sector’s historic players.

The financialization of collection also changes the game

Another movement, less visible but more systemic, is playing out on the side of the for-profit U.S. collective management organizations. As of mid-2026, BMI is controlled by New Mountain Capital, SESAC by Blackstone and GMR by Hellman & Friedman, while ASCAP remains the independent mutual exception.

This development creates a new verticalization linking capital, collection and catalog. When a single financial sponsor can control a collection channel and, directly or indirectly, a stock of rights whose revenue depends on that collection, the boundary between market infrastructure and exploited asset becomes far more porous. In the investigation, this is presented as the principal systemic risk of the 2026–2028 market, more so even than the question of multiples alone.

A two-tier market

The new mapping leads to a distinctly bipolar market structure. At the top, a handful of global players — majors, independent quasi-majors and large financial sponsors — compete for rare assets above several hundred million dollars. At the base, the sharpest growth concerns instead the long tail, small deals and emerging geographies, where the Music Finance Index observes the most favorable expectations by volume.

This bipolarization has a direct consequence for sellers and intermediaries alike. A catalog no longer enters “the market” in the abstract: it enters a precise sub-market, defined by its size, its geography, its cash-flow profile, its possible uses and the type of buyer best able to extract the most value from it.

This is probably the essential lesson of the sequence. The catalog market is neither simply bigger nor simply more expensive: it has become more legible if one reads it as an architecture of vehicles, capital profiles and operating intensities rather than as a list of spectacular deals.

This article summarizes a section of a ~45-page professional report by @music_zone, which outlines the 2024–2026 cycle of catalog acquisitions:

– the Hipgnosis/Recognition deal and its financing;

– the new landscape of acquirers (majors, BMG-Concord, funds, non-English-language labels);

– valuation benchmarks (Shot Tower, Music Finance Index) and the stabilization of multiples at a plateau rather than the predicted collapse;

– growth drivers (licensed AI, superfans, derivative rights, non-English-speaking markets) and the risks of concentration in capital, revenue, and catalogs.